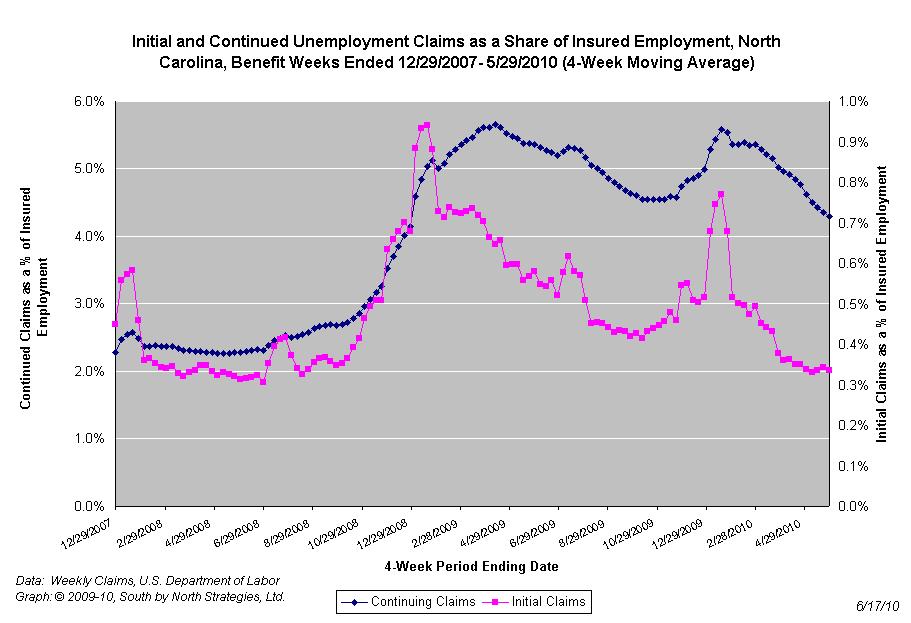

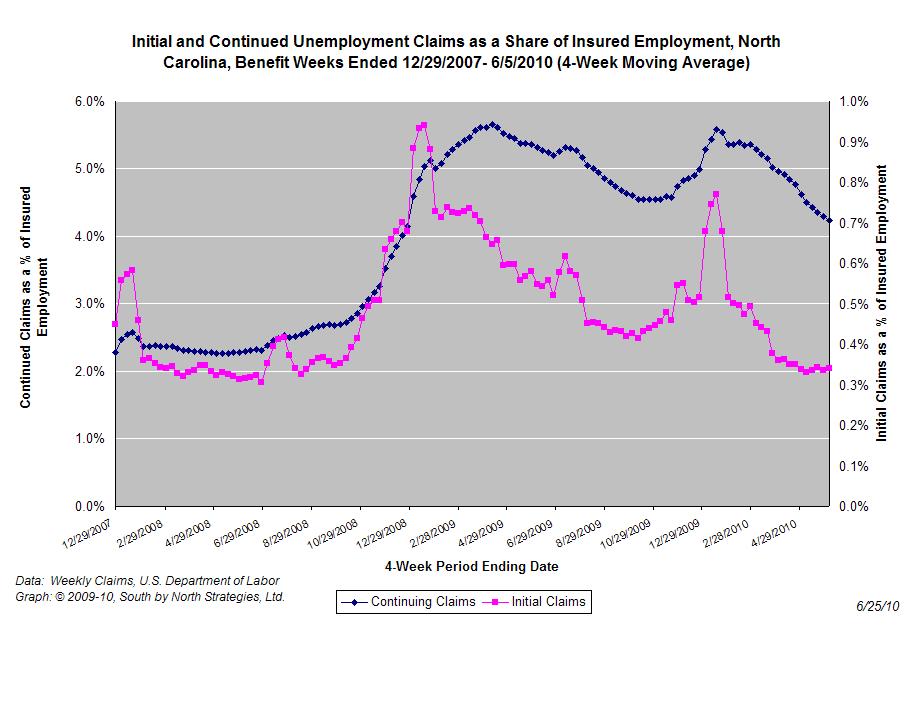

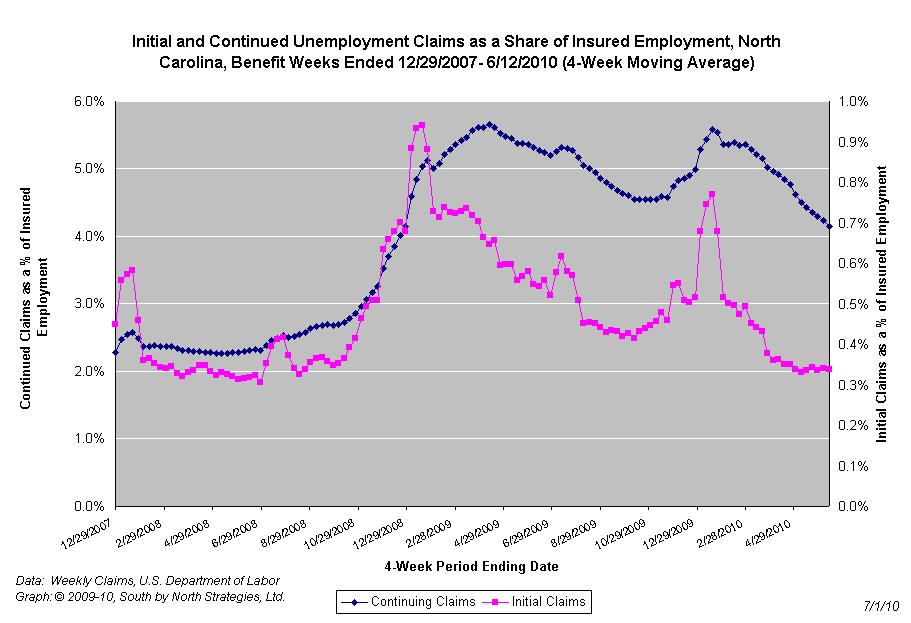

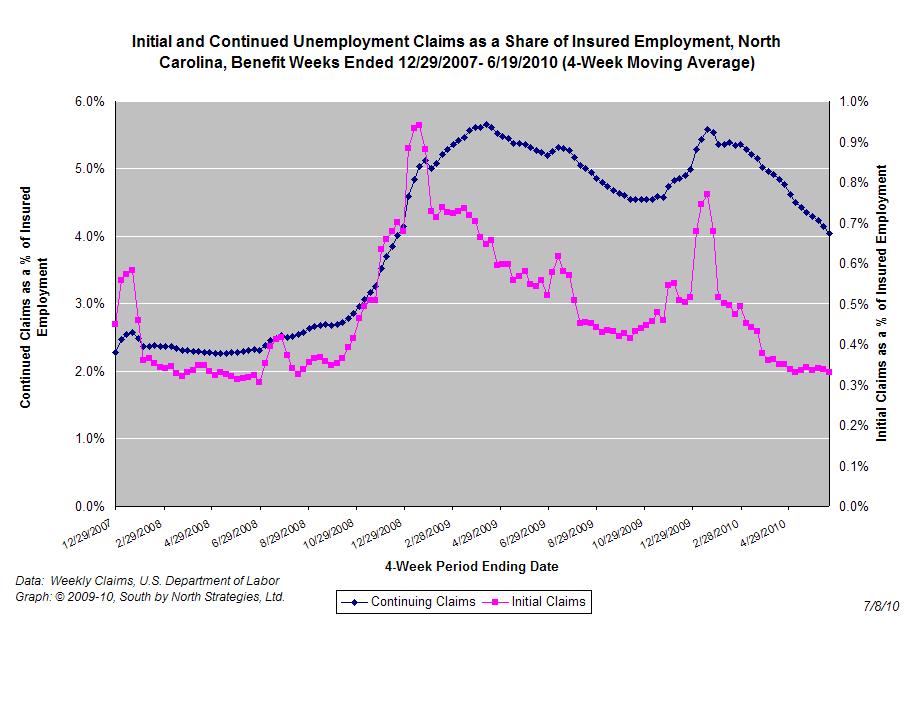

A Weak National Jobs Report for August

CHAPEL HILL (September 3, 2010) – The national employment report for August contained little good news. Last month, employers eliminated 54,000 more payroll positions than they added. An expected fall in temporary census employment drove that decline; after accounting for it, the economy netted 60,000 positions, a level insufficient to either keep pace with workforce growth or re-absorb jobless individuals.

“The basic employment picture was unchanged in August,” said John Quinterno, a principal with South by North Strategies, Ltd., a research firm specializing in economic and social policy. “Payroll employment fell due to the ending of temporary census positions. When those jobs are excluded, the nation netted just 60,000 payroll positions, virtually all of which were in the private sector.”

In August, the nation’s employers shed 54,000 more payroll positions than they added. Losses occurred primarily in the public sector due to the elimination of 114,000 temporary census jobs. When census reductions are excluded, the economy netted 60,000 positions. One positive development was that payroll employment numbers for July were revised upwards; with the revision, the economy lost 54,000 jobs in July rather than the 131,000 positions initially reported.

The largest private-sector gains in August occurred in education and health services (+45,000), professional and business services (+20,000, with most of the gains occurring in the temporary help services sub-industry), and construction (+19,000). Manufacturing payrolls fell by 27,000 positions. Additionally, the public sector slashed 7,000 positions in addition to temporary census jobs.

“The August employment report offers little evidence that a meaningful labor market recovery is underway,” noted Quinterno. “The private-sector simply is not generating jobs at a level needed to accommodate all those individuals who wish to work.”

Weak conditions were reflected in the August household survey. Last month, 14.9 million Americans (9.6 percent of the labor force) were jobless and actively seeking work. Proportionally more adult male workers were unemployed than female ones (9.8 percent vs. 8 percent). Similarly, unemployment rates were higher among Black (16.3 percent) and Hispanic workers (12 percent) than among White ones (8.7 percent). The unemployment rate among teenagers was 26.3 percent.

Furthermore, newly available data show that 8.7 percent of all veterans were unemployed in August; the rate among veterans who had served since September 2001 was 9.4 percent.

“There currently is a great deal of unused labor in the American economy,” added Quinterno. “Compared to a year ago, the labor force is smaller, fewer people are employed, and the unemployment rate essentially is unchanged. Employers also have many options that they can use before hiring additional help, such as by giving hours to current employees on shortened schedules.”

Jobs remained hard to find in August. Last month, 42 percent of unemployed workers had been jobless for at least six months with the average spell of unemployment lasting for 33.6 weeks. Many other individuals stopped looking, and counting those individuals and those working part-time on an involuntary basis brings the underemployment rate to 16.7 percent.

“The reduction in temporary census hiring over the summer exposed just how weak the labor market really is,” observed Quinterno. “While private employers are not slashing jobs at the ruthless pace of late 2008 and early 2009, they are not adding positions in any meaningful way. Many Americans who are ready, willing, and able to work are finding themselves boxed out of the job market.”

Email Sign-Up

Email Sign-Up{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}